Summary

Key Takeaways:

Geopolitics continue to gyrate markets with the recent ceasefire seen as an untenable resolution, could the U.S. leave the world to deal with the fallout?

Positioning driving cotton rally - Spec positioning is now -10,000 lots while Commercials have built a net position of -85,000 lots

US Cotton exports are improving and if continued the USDA will likely have to adjust their forecast for 25/26.

Coffee supported by strong diffs, tight nearby supply, and firm spreads.

Farmer selling delayed - Brazil/Colombia producers well capitalised and holding back supply and waiting for a rally in flat price.

Medium-term pressure remains - coffee likely to soften as new crop arrives and supply normalises.

A two-week US-Iran ceasefire, brokered by Pakistan just before Trump's deadline expired, triggered a broad relief rally oil plunged roughly 16–17% back below $95/bbl, the Dow surged ~1,300 points for its best session since April 2025, and Treasury yields fell sharply as rate-cut odds jumped from 14% to above 43%.

WTI had rallied 69% and European natural gas 61% over the six weeks of conflict since hostilities began on 28 February so the unwind was dramatic. Iran's 10-point proposal includes demands for sanctions relief and acceptance of its enrichment program, while Israel is pressing for deeper concessions including surrender of enriched uranium stockpiles.

The a two-week pause is not a resolution and markets will remain sensitive to any breakdown in talks. Iran's parliamentary speaker has already accused the US of violating the ceasefire, and tanker traffic through the Strait reportedly ceased after an Israeli strike on Lebanon. Fighting could reignite later this year or even later this month, leaving energy and commodity markets on a structurally higher floor as governments hoard and restock in anticipation of renewed hostilities.

Cotton rallied to its highest since December 2024, with May futures hitting 71.93 c/lb as traders weighed the USDA prospective plantings report against tighter global supply expectations. Support came from elevated petroleum prices lifting input and shipping costs as well as raising polyester prices,

while hot, dry weather persists across US cotton areas from Texas westward. Weekly export sales were strong at a combined 488,746 RB (old + new crop), the highest in six weeks, led by Vietnam and Turkey, though the ceasefire-driven oil crash on Tuesday/Wednesday may unwind some of that energy-cost tailwind.

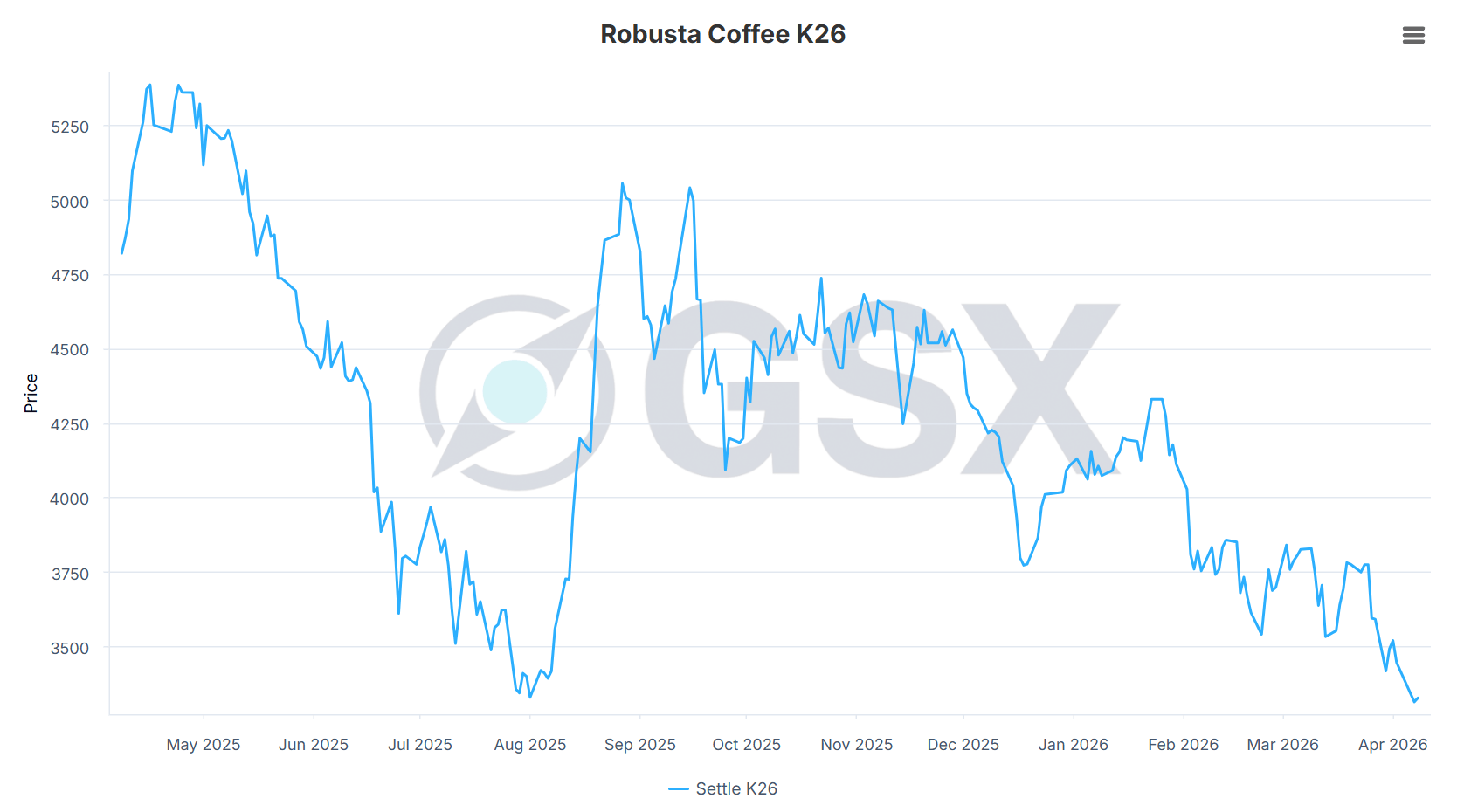

Coffee sold off hard into the ceasefire. May arabica dropped 4% on Tuesday to 286.1 c/lb, marking a third consecutive session of losses, while London Robusta fell 3.86% to $3,315/ton. The bearish driver remains the supply outlook. StoneX projects a record 2026/27 Brazil crop of 75.3 million bags and a global surplus expanding to 10 million bags, the largest in six years. Vietnam's March customs-cleared exports rose 25% y/y to 222,000 tonnes adding further pressure to flat price for Robusta. The ceasefire should ease freight and energy cost pressures that had been supporting the flat price, likely keeping arabica under pressure near-term unless the truce collapses.

Cotton

Cotton Price Action

May futures rallied to 71.93 c/lb last week, the highest since December 2024 flat price has been supported by elevated energy costs lifting polyester prices and hot, dry weather across Texas. The May/July spread narrowed modestly as the front month gained 46 points on the week, with July trading around 73.05 c/lb, maintaining a carry structure reflecting adequate nearby availability against tighter deferred expectations. Combined old and new crop export sales hit 489,000 RB, a six-week high led by Vietnam and Turkey, though the ceasefire oil crash may unwind some energy-cost support.

ICE Cotton No.2 front month:

Spreads (N/Z):

Cotton Positioning

CFTC Managed Money: Managed Money has reduced its short position as the market has rallied. It is likely they are going to approach a net position close to zero. While Commercials continue selling into the rally selling 19k during the last reporting period.

US Cotton Export & Sales

US Cotton Exports, continue to be strong, with pace picking up over the past two weeks. We project that the U.S. will export ~11.82 million bales, which is an increase of 0.22 million bales since our last report.

If this trend continues and pace accelerates further, our projections will likely be revised higher, potentially exceeding 12 million bales. We don’t expect this to be in the April WASDE however adjustments to exports are more likely in the May and June WASDE.

Despite this we don’t expect this to have a major impact as the carryout is still very high and new crop cotton production, based on current planted acres, is expected to add 0.35 million bales.

Cotton On-Call

No major outliers in the report other than there remains a large number of OC purchases in the new crop December contract.

Outlook for Cotton

Bull Case

BACA is passed and the current crop US balance sheet is impacted

Dry weather and low subsoil moisture causing abandonment in Texas and the U.S. in general

High Urea costs causing issues with the crop

Continued strong exports out of the U.S. lowering the carryout

The war in Iran continues

Bear Case

Demand takes a further hit from the war in the Middle East

Synthetic fibres continue to gain market share and PSF pricing fall.

Weather is perfect in Texas and the United States

Cessation of hostilities in the Middle East

Base Case

Whilst spreads stay in a wide carry, speculators have little incentive to go long the market and every incentive to stay short. While the bears have been forced to cover there is still a high probability that this short could be reignited if the carry in the market is not reduced.

The key metrics to track will be the crop progress and we await the results and what look out for opportunity in the 2nd half of the year.

Coffee

Coffee Price Action

May arabica fell 4% on Tuesday to 286.1 c/lb, a three-week low, with robusta dropping to $3,315/ton, an eight-month low, as record Brazilian crop forecasts (StoneX at 75.3m bags, 10m bag global surplus) and surging Vietnamese exports (+25% y/y in March) weighed heavily. The K/N spread remains elevated in backwardation, reflecting tight nearby certified stocks even as the forward curve prices in the incoming supply glut. The Iran ceasefire has removed the freight and energy premium that had been supporting the flat price.

ICE Arabica front month:

ICE Robusta front month:

Arabica K/N:

Robusta K/N:

Physical Pricing

Brazil differentials: Robust has come off dramatically, whilst Arabica stays strong.

Central American and Colombian Diffs continue to strengthen

Indonesian and Vietnamese diffs are flat WoW

Certified stocks: Arabica certs are stable while Robusta continues to decline slightly.

Coffee Positioning:

For Arabica CFTC Managed Money: Longs have gradually been building up their long position while commercials have continued to sell.

For Robusta CFTC Managed Money: MM sold while MM bought during the recent volatility.

Exports:

Brazil and Colombia export pace: Much slower YoY due to smaller crop, tariffs and high differentials.

Honduras and Indonesian Export pace: Honduras has been shipping more coffee faster this market year due to a favourable basis and weaker currency.

Vietnam exports: Exports are healthy as demand ahead of the arrival of Conilon. Uganda has been overall strong this market year.

Outlook:

Bull Case

Weather shock in Brazil (frost, drought) cuts 2026/27 off-year yields further as the market already structurally vulnerable

Geopolitical risk premium pulls passive/macro money into commodities complex

Curve deepens into backwardation leading to Sep/Dec spreads rally and causing CTAs and specs add length, amplifying flat price move

Roasters caught short coverage forced to chase if the 75m bag crop misses

Basis rallies alongside flat price as nearby supply remains constrained

Bear Case

Brazil 2026/27 crop comes in on schedule and Arabica output potentially up to ~50m bags

Rabobank sees a surplus of 8.6m bags in 2026/27, projecting Arabica prices down ~ a third by late 2026

Brazilian farmer capitulates on old crop and export volumes surge after a 20% YoY decline in 2025

US tariff removal normalises Brazilian trade flows, roasters return to regular procurement

Iran conflict short-lived, oil normalises, freight and insurance ease, cert stock rebuild accelerates

Curve flips to contango, carry economics improve, CTA money reverses, flat price grinds lower

Base Case

Closer to bear case, but the market won't fully price 2026/27 supply until new-crop harvest is confirmed

Near-term focus on Sep/Dec and Dec/Mar spreads, curve shape is the leading signal

Elevated Brazilian and Colombian diffs look like a structural short rather than genuine scarcity; expect compression once new-crop volumes arrive

Conilon diffs are an important signal, once farmers see crop viability, diffs collapse; same dynamic likely for Arabica with a lag

Roaster coverage currently above 2025 average, limits demand-driven spikes in nearby contracts

Base trajectory: cert stocks rebuild gradually, diffs compress on harvest, flat price drifts lower as surplus outlook firm’s diffs and we would expect this to ease when the new crop harvest arrives.

Appendix: